Understanding Contribution Factor: A Practical Guide to Profitability

Contribution factor reveals whether to scale or stop, helping founders distinguish broken unit economics from businesses that simply need more volume.

Framework

Framework

Problem statement: Many businesses struggle with persistent losses, trying every conventional fix (cutting costs, freezing hiring, slashing marketing budgets) only to watch losses continue or deepen. Sometimes making a business profitable and scaling it is not an operational problem but a simple finance puzzle to be solved. Calculating the contribution factor can reveal whether the business model itself works or is fundamentally broken. Understanding and acting on this one metric can make a whole business succeed and ignoring it can turn a promising venture into a lost stock.

What is Contribution Factor?

The contribution factor is the amount of money left over from each sale after paying the variable costs of making that sale. That leftover is what “contributes” toward covering the fixed costs of the business and once fixed costs are covered, everything beyond it is profit.

Two definitions are needed to read the formula correctly:

- Variable costs change with every unit sold — cost of goods, packaging, shipping, payment fees, and performance marketing.

- Fixed costs do not change with sales volume in the short run — rent, salaries, software, leases.

Performance marketing is a variable cost, not a fixed overhead. Misclassifying it is the most common reason businesses cut marketing when they should be increasing it.

The Formula

Worked example: If a product sells for a certain price and the variable cost per order is lower, the contribution factor is the difference. Each order contributes that amount toward covering fixed costs. Once total contribution exceeds monthly fixed costs, the business reaches break-even. Every order beyond that point is profit.

Why does Contribution Factor Matter?

The contribution factor answers the most important strategic question in any struggling business: should we add more volume, or stop?

- If it is negative: every sale loses money. Scaling makes the loss bigger. Fix unit economics first.

- If it is positive but volume is low: the model works; the business is simply too small to cover its fixed costs. The right move is to grow into the cost base by spending more on marketing, not less.

- If it is positive and volume already covers fixed costs: defend margins and reinvest selectively.

Case Study: Treya Gifts

The Company

Treya Gifts is a Direct-to-Consumer e-commerce brand selling STEM (Science, Technology, Engineering, Mathematics) educational toys for kids across India. The brand had built a loyal customer base and strong product reviews, but growth had stalled.

The Situation

After eighteen months of failed growth attempts, Treya Gifts came to the IBR Strategy Team. Revenue had plateaued with consistent monthly losses. The founders had responded the way most struggling businesses do: they tried to cut their way to profitability. Marketing budgets were slashed, discretionary spending was frozen, and every variable cost line item was scrutinised and trimmed.

The logic seemed sound: if the business is losing money, reduce costs. But each round of cuts was followed by proportionate drops in orders, and losses persisted. The founders were considering shutting down the business.

The Diagnostic

The IBR Strategy Team started by analysing the balance sheet and rebuilding the P&L on a per-order basis. The objective was not to find more costs to cut, but to answer a foundational question: does each individual sale create value or destroy it?

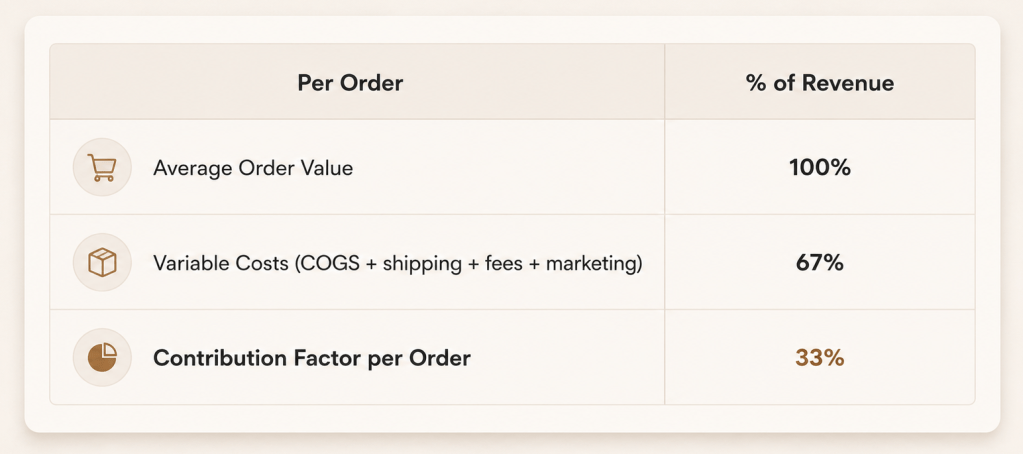

The contribution factor was clearly positive at 33% of revenue. This was the critical insight. Treya was not selling at a loss. Every order was contributing toward covering fixed costs. The business model worked. The problem was scale, not economics.

With monthly fixed costs (rent for warehouse space, salaries for the core team, and essential software), the business needed to reach a certain order volume to break even. Treya was operating below that threshold. The fixed cost base was too large relative to current volume, creating a net loss. But because the contribution factor was positive, every additional order moved the business closer to profitability, not further away.

The founders had been cutting variable costs to reduce losses. This was making the problem worse. Lower marketing spend meant fewer orders, which meant the same fixed costs were spread across an even smaller revenue base, deepening the loss.

The Recommendation

The IBR Strategy Team recommended the exact opposite strategy: increase variable costs, specifically marketing spend, until total variable costs comfortably exceeded the fixed-cost barrier. The logic was straightforward. Since the contribution factor was positive, every rupee spent on acquiring an order at the current unit economics brought in contribution margin. Scaling volume would increase total contribution margin faster than fixed costs, pushing the business past break-even and into profitability.

Three guardrails were attached to prevent runaway spending:

- Marketing cost per order was capped safely below the contribution margin per order to ensure every incremental order remained profitable.

- Channel mix was rebalanced toward performance-based channels with clear per-order attribution, so contribution factor could be tracked in real time.

- Fixed costs were frozen — no new hires, no warehouse expansion, no discretionary infrastructure spend — until order volume stabilised at the new level.

The Result

The business executed the recommendation over a twelve-week period. Marketing spend increased significantly. Orders grew 180%, and revenue scaled proportionately.

Three critical outcomes validated the strategy:

- Contribution factor per order held steady at 33%: confirming that the additional marketing spend was acquiring profitable customers, not buying revenue at a loss.

- Total contribution margin increased proportionately with volume: which is exactly what a positive contribution factor predicts.

- Total contribution margin surpassed the fixed cost barrier: the contribution margin comfortably covered the fixed cost base, creating sustainable operating profit. The business had crossed break-even and was now sustainably profitable.

Fixed costs grew only 8% which is a modest increase to accommodate slightly higher transaction volumes and customer support load, but the core team and infrastructure remained frozen as planned.

Treya Gifts moved from monthly loss to monthly profit in three months, not by cutting costs, but by spending more on the right line item. This is the contribution factor in action.

The Lesson

Treya Gifts was doing everything operationally right: good product, strong retention, clean execution. What looked like a struggling business was actually a sub-scale business with sound unit economics. Without the contribution factor lens, the founders would have continued cutting variable costs, shrinking volume, and wondering why the losses persisted. With it, the path to profitability was immediate and mechanical: increase variable spend until contribution margin exceeds fixed costs. This is how companies doing everything perfectly can still struggle without the right financial strategy.

The author of this Review

Vivek Bisht

Serial entrepreneur and advisor working at the intersection of technology and business. Has built growth engines for 15+ brands across D2C, SaaS, and services, shaping how modern companies scale. Leads Ikana’s strategic thinking, developing original frameworks and execution models.

Leave a Comment

Related Reviews

The Inverted Launch for AI (ILA): Why AI Products Launch Differently

Why successful AI products launch multiple tools, measure real user pull, remove underperformers, and scale only the capabilities the market…

$139 spent on X vs Meta vs LinkedIn Ads (The Good, The Bad & The Ugly)

My experiments with X, Meta, and LinkedIn campaigns to verify platform marketing claims.

The GEO Metrics to Track Your Growth in 2026

With an increase in AI results and putting in efforts for GEO, how do you really measure it?

GEO Marketing: Why Search Is Becoming an AI Answer Layer

AI is replacing search results with synthesized answers. Learn why visibility now depends on being selected, cited, and trusted (not…

Please sign in to leave a comment.